Accompanying a Spanish bank on its sustainability journey propelled Metyis to innovate new ESG capabilities

The priority of climate and environmental awareness has reached an all-time high in recent years.

The financial sector has been pivotal in promoting an energy transition across all economic strata through green financing and financial innovation options. To comply with the Paris Agreement, which aims to contain global warming well below 2ºC by the end of the century, the European Commission estimates the EU needs €0.35 billion per year until 2030. The financial sector’s role is crucial to reaching this goal. Financial companies are increasing efforts to confront sustainability challenges, understanding that to minimise Environmental, Social and Governance (ESG) risks and release the full potential of new opportunities, they must raise internal awareness and address reputational considerations with stakeholders. Furthermore, companies will have to comply with a regulatory and supervisory tsunami to adapt their structures, procedures, and business models.

The EU's regulatory and supervisory framework consists of three main pillars (Diagram 1):

- The Energy Union, the strategy for the energy sector transition and the mechanism responsible for ensuring compliance with the Paris Accord's targets.

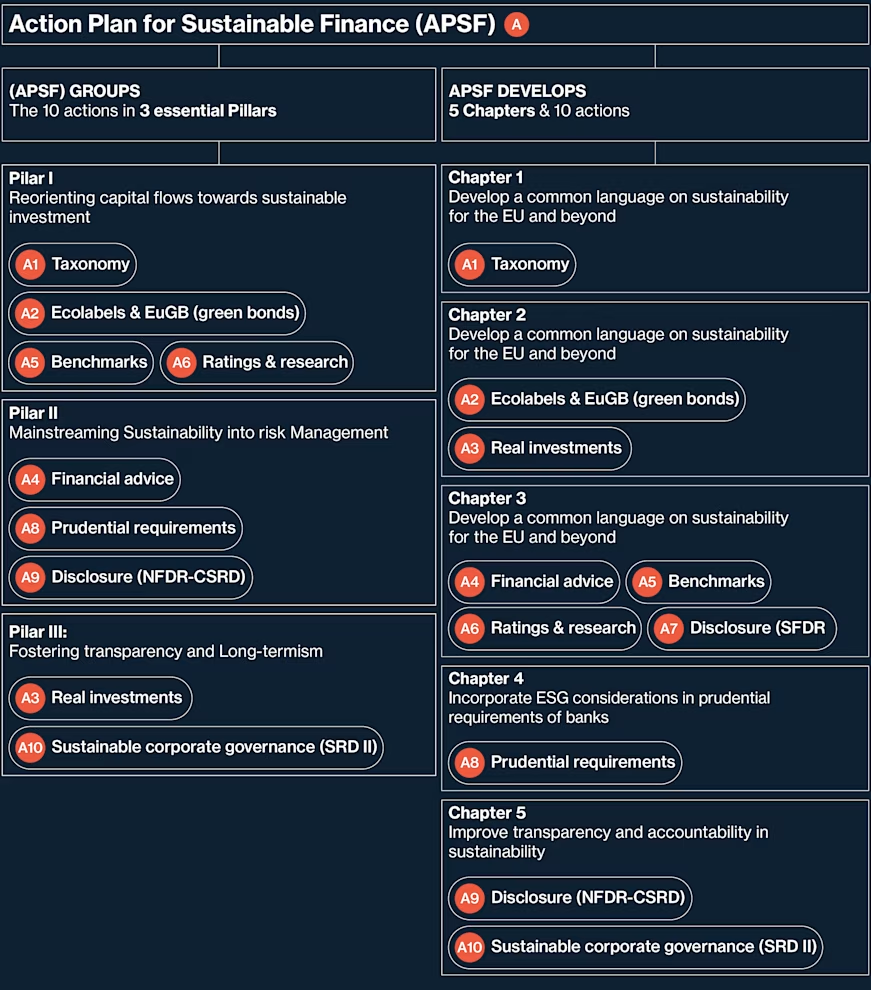

- The Action Plan for Sustainable Finance (APSF)2, the guideline for developing sustainable finance (Financial flows and instruments with ESG considerations).

- The European Green Deal (EGD)3, the roadmap for transforming production and consumption patterns in economic sectors to increase sustainability.

Inspired by dozens of regulations, guidelines and recommendations, the European Commission published The APSF in March 2018 (amended July 2021). It is the EU's strategy for an ESG transformation of the financial sector and promoting sustainable finance. It consists of five pillars and ten additional actions aimed at linking finance and sustainability (Diagram 2). It contains a profound financial regulation reform to meet three main objectives:

- To increase and redirect capital flows to sustainable investment.

- To manage financial risks arising from climate change and energy transition.

- To foster transparency and longtermism in both finance and the economy.

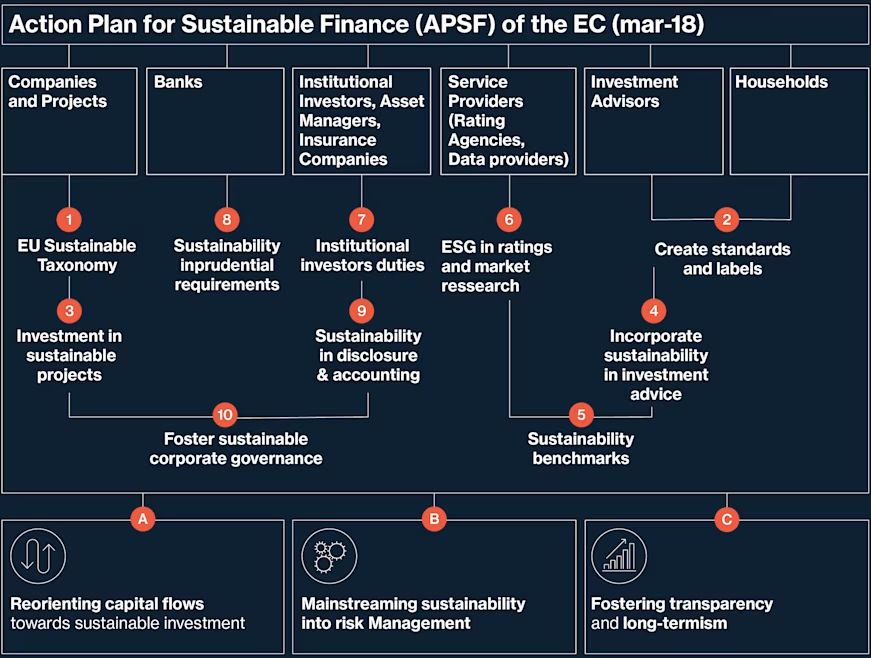

The APSF is ambitious and tackles several issues and impacts on multiple actors (Diagram 3). In one respect, it affects households and investment projects of non-financial companies. Conversely, it impacts financial companies, such as banks, investment advisors or institutional investors (insurance undertakings, asset managers), and financial services companies (data vendors, rating agencies, index providers).

The new ESG to-do list for financial and non-financial companies

There are substantial challenges for economic actors, which are increasing on different fronts:

Sustainable finance product development (actions 1, 2, 4, 5 & 7 APSF)

Financial actors have the mission, responsibility and incentive to "green" their products and redirect capital flows from "brown" toward sustainable activities. For this to happen, they must manufacture a short and stringent list of officially "sustainable finance products" (A1 & A7). These products would then be distributed to end-investors with ESG preferences (A4) and be part of ESG market indexes (A5). Financial actors can also finance themselves by issuing European green bonds (EUGB) and supporting non-financial companies' bond issuance.

ESG Reporting (actions 1, 6 & 9 APSF)

On an annual basis, financial companies can extract, interpret and integrate all relevant sustainability disclosures of companies which are part of their investment products (A9), including their alignment with EU Taxonomy (A1). To assist in digesting this new information, they can rely on ESG ratings provided by rating agencies (A6).

Risk management and governance (actions 7, 8 & 10 APSF)

Financial actors must take into account sustainability considerations in their internal governance setup (A10) and consider ESG risks and factors of investment companies (A7). Most importantly, they must contemplate ambitious changes in their structure and operations, especially in banks and insurance companies (A8). These changes may arise from both stakeholders' "soft pressure" (market dynamics or demands from other companies, consumers, or society as a whole) and "hard pressure" exercised by regulatory requirements and supervisory expectations.

Non-financial companies face new ESG requirements in almost all sectors, especially mid to large-sized companies:

Sustainable financing (actions 1, 2, 5, 6 & 7 APSF)

Companies may issue green bonds (A2), which have stringent requirements owing to an alignment with EU Taxonomy (A1). They may issue "traditional" equity, but market pressure and volatility may increase if they fail to show good ESG performance. In many ways, becoming ESG resilient may give companies lower funding costs as well as competitive advantages, such as higher ratings (A6) or inclusion in ESG indexes (A5) and sustainable finance products (A1 & A7).

ESG Reporting (actions 1, 7 & 9 APSF)

Non-financial companies must disclose ESG information in their annual management report (A9). This information becomes essential for the Action Plan, especially in creating sustainable finance products (A1 & A7). Furthermore, new and increasing requirements are now in place regarding EU Taxonomy. Under the perimeter of the EU Taxonomy, companies must make annual publications of their degree of compliance regarding CapEx, Opex and sustainable activities. The higher their alignment, the greater the financial and reputational benefits, which translates into better funding and growth prospects. This set of incentives is progressively evolving, offering the potential to foster new business models better oriented towards sustainability.

Lessons learnt and developments made: a case study of Metyis' role in guiding a client to ESG success

The challenge

A mid-sized Spanish bank hired Metyis to partner in developing tools and improving its ESG positioning and performance. Some of the identified priorities were the following:

Metyis helped identify some priorities

1. To increase the understanding and awareness of sustainability challenges faced by the bank. Metyis analysed dozens of studies, recommendations, and regulations to create reports and presentations on the ten actions of the APSF. These resources, updated regularly, were distributed through the internal teams' channel (including around 500 top and middle managers) and presented to different internal committees.

2. To develop tools to analyse the vulnerability of transition risks in the loan portfolio. Metyis helped the risk management department implement a transition risk methodology for the bank as part of the United Nations Environment Programme Finance Initiative (UNEP-FI)6. In this instance, Metyis used an Input-Output Methodology and expanded it with a framework for embodied-carbon emissions. The objective was to add value-chain considerations to emissions output in each Spanish sector.

3. To create an internal climate risk policy. Metyis developed a proposal for managing, controlling and mitigating climate risks (both physical and transitional). The proposal identifies the people in charge of surveillance, tools and goals. This policy was a requirement imposed by supervisors (the European Banking Authority under the EU institutional ecosystem and the Single Supervisory Mechanism of the ECB under the euro umbrella). It was finally approved internally in the bank by the competent body.

The impact of Metyis' role

Throughout the process, Metyis assisted the bank with sustainability, regulation, risk management, and financial management whilst developing internal capabilities for aiding current and prospective clients, both financial and non-financial. The new capabilities have strengthened Metyis’ sustainability services, created new client proposals and reinforced the relationship with the bank, which externally published several articles on the work in influential Spanish policy think tanks.

Enterprises worldwide require urgent guidance as they navigate sustainability and comply with new regulations. The financial sector is instrumental in funding ESG projects, and Metyis gained invaluable knowledge of its inner workings when assembling a Spanish financial institution’s ESG strategy. Metyis holds a roadmap to ESG excellence that can be adjusted to meet various enterprises’ needs.

Miguel Solchaga is an experienced consultant in multinational environments with wide expertise in strategy, marketing and economic consultancy projects across different industries, including financial services, energy and FMCG. He is a partner in the Madrid office.